A Spotlight On Depreciation

Published September 6, 2016

Appreciation of depreciation can prove very valuable for those with investment properties or small businesses. So what is depreciation and what and how can you depreciate?

According to the ATO definition, a depreciating asset is an asset that has a limited effective life and can be expected to lose value over time. As such, you can depreciate the cost of the asset over its life and this can then reduce your tax liability. It could even turn a tax bill into a refund cheque.I

When it comes to investment property there are two types of depreciation – the building structure or capital works allowance (Division 43) and depreciating assets such as ovens, flooring and light fittings (Division 40).

Assets depreciate much faster under Division 40 than Division 43. Generally, it's easy to determine into which category the asset falls but there can be some confusion. For instance, you can claim an air conditioning unit under Division 40 but ducting for that unit would fall under Division 43.ii

Rates Of Depreciation

When it comes to depreciating the building structure, as long as the property was built after 17 July 1985, you can depreciate it at 2.5 per cent a year over 40 years. The property does not even have to be new when you buy. Say you bought a property in 2016 that was built in 1995, you could still depreciate it over the next 19 years.

With depreciating assets, the rate of depreciation will depend on the item. And the rate is actually determined by the ATO.

Your choice of a particular asset, say a floor covering, can impact on the depreciation. For example, a carpet will actually have a shorter effective life than tiles. As a result, you can depreciate a carpet much faster and so the benefit will be greater.

Other items that can be depreciated include ovens, dishwashers, curtains, air conditioners and hot water systems.

According to the ATO definition, a depreciating asset is an asset that has a limited effective life and can be expected to lose value over time. As such, you can depreciate the cost of the asset over its life and this can then reduce your tax liability. It could even turn a tax bill into a refund cheque.

Ways To Depreciate

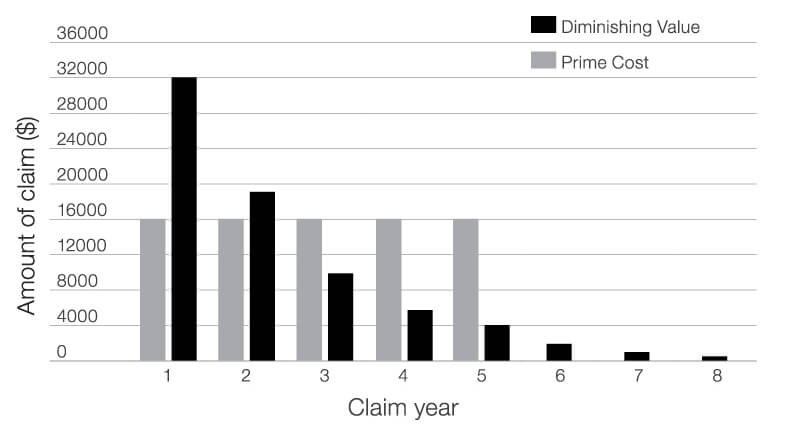

There are two ways to depreciate assets – the prime cost method or the diminishing value method.

With the prime cost method, you depreciate the value of the asset evenly over its effective life. In contrast, the diminishing value method allows you to depreciate the item more in the years immediately after purchase.

The method you choose will depend on your circumstances. If you want to minimise your tax deductions, then the prime method might be better for you. If you want to claim more deductions in the early years, then you might choose the diminishing value method.

Diminishing Value or Prime Cost?

Source: ATO

Choosing which method can be a complex exercise. As a result, it might be a good idea to engage the services of a quantity surveyor to prepare a depreciation schedule.

This will provide a detailed inventory of your depreciating assets and any capital work allowances. It will then compare the valuation methods and we can help you decide which one most suits your particular circumstances.

It's a smart move if you want to make sure that you capture everything that you are allowed to depreciate.

Assets that are worth less than $300 can be immediately written off rather than depreciated over a period of years. However, if you bought a set of four chairs at $180 each, you wouldn't be able to write off each chair individually. The four chairs would be treated as one item worth $720 and depreciated over time according to the depreciation schedule.

Whenever you make changes to your investment property such as renovating the kitchen, you need to consider the items you discard. When you remove a depreciating asset from a property, you can actually take advantage of "scrapping" which is where you write off the residual value of the asset in one hit.iii

And once the renovations are complete, you can create a new depreciation schedule for all the new assets.

If you realise that you have not been depreciating your assets, the ATO will allow you to back claim depreciation for up to two years.

Small Business Depreciation

In 2015, the ATO changed the depreciation rules for small businesses with turnovers of less than $2 million in a bid to simplify the process.

Under the new system you can immediately write off any depreciating asset that cost less than $20,000. When items are worth more than $20,000 you can pool them and claim a 15 per cent deduction in the first year and a 30 per cent deduction each year afterwards.

When working out deductions not only can you include the actual price of the asset but also any additional amounts you have spent on transportation and installation.

Of course you can only deduct the part of the asset that is used in your business, so you will need to calculate how much that is.

If you want to know more about how you can use depreciation to better your financial situation, then call us to help you make the most of your allowable deductions.